The state budget of Georgia includes reserve funds, the purpose of which is to cover unforeseen expenses incurred during the year. As with the state budget, reserve funds are also included as part of the budgets of local self-government units.

The state budget of Georgia includes reserve funds, the purpose of which is to cover unforeseen expenses incurred during the year. As with the state budget, reserve funds are also included as part of the budgets of local self-government units.

The reserve fund of a local self-government unit encompasses the funds allocated by the municipal budget for the purposes of financing unforeseen, emergency, and other events of local importance.Therefore, the purpose of the reserve fund is to cover expenses incurred during the year that could not be taken into account due to objective circumstances in the budget planning process, such as natural disasters, epidemics, environmental and other disasters. Consequently, the situation created by the Covid-19 virus pandemic in 2020 necessitated the financing of certain measures to fight the virus from the reserve funds.

IDFI studied the practice of spending the reserve funds of local self-government units in 2020. The analysis of the expenditure of the reserve funds discussed in the study is based on the data reflected in the budget spending reports of the municipalities. The study also utilized information on current expenditures from reserve funds that had been requested from municipalities in September 2020. Out of 64 municipalities, 9 municipalities left IDFI's request regarding the reserve funds unanswered. Specifically, the city halls of the municipalities of Adigeni, Akhalkalaki, Akhmeta, Akhmeta, Bolnisi, Lanchkhuti, Lentekhi, Sighnaghi, Shuakhevi, and Kharagauli neglected the obligation to provide public information as prescribed by the legislation of Georgia.

It should also be noted that, in the case of 6 municipalities, the information provided to IDFI regarding the expenditures from the reserve funds was incomplete.For example, the mayors of Chokhatauri and Tsalka provided IDFI with only a list of measures for which funds were allocated from the reserve fund, although no information was provided on the precise allocation of funds for each of these.In other cases, the municipalities did not indicate the exact purpose of the funds spent from the reserve funds.

The research process was also significantly complicated by the inconsistent practice of accounting for expenditures from reserve funds by local governments in 2020.In particular, within the context of the pandemic, a program of emergency measures was created in the budgets of individual municipalities, where a certain part of the funds was allocated from the reserve funds. As a result, the information on the expenditures from the reserve funds under the new program were inconsistently reflected in the narrative of the budget spending reports as well as in the information provided to IDFI.

Given these circumstances, IDFI analyzed information on expenditures totaling GEL 14.7 million from the reserve funds of 54 municipalities.Among them, in the case of 48 municipalities, it was possible to break down the expenditures from the reserve funds into specific categories.Namely, the analysis covers issues such as: funds allocated for financial assistance, funds for the fight against the Covid-19 pandemic, funds allocated to compensate for damage caused by natural disasters or other accidents, funds allocated for capital works, and other costs.

- In 2020, GEL 14.7 million were spent from the reserve funds of 54 municipalities.

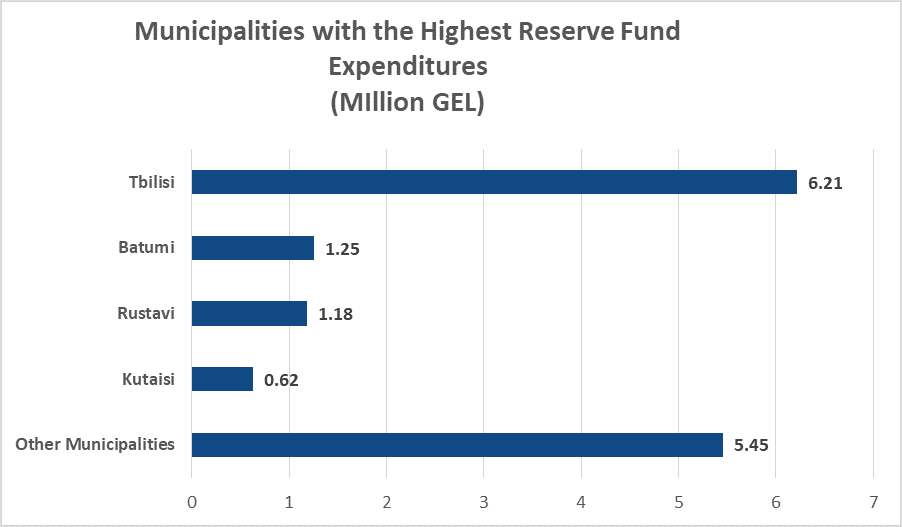

- In 2020, 63% (9.26 million GEL) of the expenditures from the reserve funds of 54 municipalities where from the reserve funds of the 4 largest cities (Tbilisi - 6.21 million GEL, Batumi - 1.25 million GEL, Rustavi - 1.18 million GEL, Kutaisi - 620 thousand GEL).

- The largest amount of expenditures from the Tbilisi Reserve Fund (GEL 2,404,700) was spent on various measures aimed at preventing the spread of the novel coronavirus.For example, a total of GEL 724,064.20 was spent to purchase anti-infectives for the protection of City Hall employees.

- In 2020, despite an increase 1.6 million in the Tbilisi Reserve Fund compared to the previous year, the reimbursement of medical expenses of citizens from the Reserve Fund was reduced by 26%, largely due to the significant amount of money being spent on various types of measures directed against COVID-19.

- 1.09 million GEL was spent on material assistance for citizens from the reserve fund of Batumi Municipality, and 151.5 thousand GEL was spent on transportation of citizens from quarantine areas.

- In 2020, the reserve fund of Rustavi Municipality grew by 836 thousand GEL compared to the previous year, which was then spent, for the most part, on activities carried out within the context of the Coronavirus pandemic.

- In 2020, about 90% (555.9 thousand GEL) of the Kutaisi Municipality Reserve Fund was spent on material assistance to citizens.

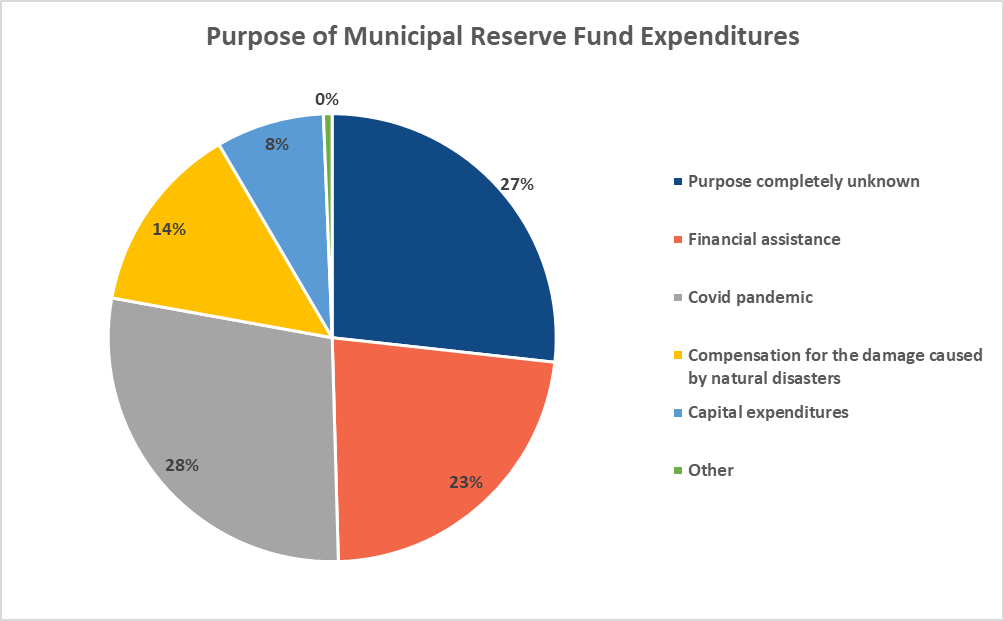

- Of the other 50 municipalities' reserve funds, 28% (GEL 1.54 million) was spent in 2020 to fund various activities aimed at combating the pandemic, 23% (GEL 1.24 million) on material assistance for citizens, and 14% (GEL 744.2 thousand) on the reimbursement for losses caused disasters or other accidents, 8% (425.4 thousand GEL) on various capital expenditures, and in the case of the remaining 27%, the purpose of the expenditures is completely unknown.

- The low utilization rates of reserve funds in a number of municipalities were a significant problem in the context of the coronavirus pandemic.For instance, no expenditures were made from the Mtskheta Municipality Reserve Fund.

- In 2020, capital projects, the purposes of which did not entail an inability to take them into account in the budget planning process and, consequently, the need to finance them from the reserve, were financed from the reserve funds of various municipalities.

- Information on the management of reserve funds by municipalities is recorded inconsistently in the budget documentation, which is mostly related to the cases of transferring funds from the budget reserve fund allocations to other program codes.

- Conflicting data on the management of reserve funds have been publicly disclosed by individual municipalities.

- The current legislation does not include important regulations pertaining to the management of reserve funds.This creates risks of misuse of finances and unsubstantiated spending of budget funds.

The analysis of the expenditures incurred from the reserve funds of various municipalities in 2020 showed that in different municipalities, the practice of determining the amount of reserve funds and their uses is significantly different.

Some municipalities incur expenditures, the need for funding from the reserve funds of which is questionable, while individual municipalities are unable to utilize the funds provided for in the reserve fund at all.The minimal utilization of the reserve fund should be assessed as particularly problematic in 2020, given the background conditions created by the coronavirus pandemic.

The inconsistent and heterogeneous practice of managing reserve funds by municipalities is clearly evidenced by the practice of allocating funds to fight the pandemic in 2020.For instance, during the fight against the pandemic, only 26 city halls expended resources from their reserve funds.At the same time, the practice of allocating funds by municipalities has little to do with the epidemiological situation in the given municipality.For example, the Batumi Municipality, where the epidemiological situation was most complicated, reduced the expenses from the reserve fund in 2020 compared to the previous year.The Oni Municipality, where no significant difficulties were observed in terms of the spread of the virus, expended resources from the reserve fund for disinfection of central streets and squares.

Incomplete regulations of the current legislation related to the management of the reserve funds can be considered a significant problem, as they createrisks of misuse of finances and unjustified spending of budget resources.Also problematic is the practice of inconsistent recording of information on expenditures from the reserve fund in the budget documentation made by a number of municipalities and the disclosure of conflicting data regarding the management of reserve funds by individual municipalities.

The transparent process of managing reserve funds is also significantly hampered by a number of municipalities refraining from disclosing detailed information on expenditures from their reserve funds. For example, most of the resources allocated from the reserve funds are directed to financial assistance to citizens. The opaque nature of this process poses significant risks in terms of unfair distribution of budget funds.

/public/upload/Analysis/ENG Spending of Reserve Funds of Local-Self Governments in 2020.pdf

The study was prepared within the grant for Good Governance for Georgia (3G) project from the global philanthropic organization, Luminate. The Institute for Development of Freedom of Information (IDFI) is responsible for the content of this analysis. Views expressed in therein do not reflect the position of Luminate.

Subscribe to Our News

Subscribe to Our News